The closing line in value betting

The closing line value (CLV) is one of the most important concepts in value betting and betting in general. If you want to understand the basics of how the betting industry operates you must be aware of the closing line and its meaning.

What the closing line is and why it matters

The closing line is the final set of odds offered by bookmakers just before an event starts. It reflects the most accurate market consensus after all available information has been priced in.

Beating the closing line — meaning you consistently get better odds than the final odds — is widely used as an indicator of long-term betting skill and positive expected value.

How the closing line is used in value betting with RebelBetting

- Odds are tracked from opening to closing across bookmakers

- Closing odds are used as a benchmark for market accuracy

- Bets placed at better odds than the closing line indicate value

- RebelBetting helps users identify value bets early, before odds move

By Nenko, founder of Church of Betting

Before I dive in, allow me to briefly introduce myself. My name is Nenko and I am the author and editor of the betting blog The Church of Betting. We decided to collaborate with RebelBetting in the form of a series of articles.

Let's dive into today's topic: The closing line.

The closing line is the odds at the time an event has started. There is something special about this moment as you will find out throughout the article. Let's have a look at how the line of a bookmaker comes to be and what are the forces that move it before game time.

Video: CLV Explained

Start your free trial

Sure betting and value betting included. No credit card required.

The life of a line

A line would open at a certain time before an event starts. Different bookmakers would open at different times. The exact time of posting a line is an important decision for a bookmaker to make.

If you open first, you have the competitive advantage of offering a line that no one else offers (at least for a while). You win the action of the punters who want to bet straight away. But you have the disadvantage that you can't "compare notes" with the competition and you are therefore at risk of putting up a wrong number, which can be costly. Furthermore, it would usually be the sharp punter who wants to hit the early line.

The early line simply offers more value than the late one and sharps know that. This doubles the risk for the bookmaker.

A line being born

In general, the bookies that open first are the ones who are more confident in their ability to make a decent line. This does not necessarily mean that they fully trust their opening numbers. Yes, a wrong number can be costly, but this cost can be easily capped using betting limits. After a bookie receives a bet on their opening line, they will move the line. How much depends on the size of the bet (bigger bets would move the line more) and the history of the punter who has made it. The more respect the bookie has for the punter, the more the line will move.

After some time has passed and the bookie has collected a few bets, it is already more confident about its number and increases the limits on how much you can bet. This process repeats several times up until kick-off when generally bookmakers will offer the highest limits.

Why increase the betting limits?

This is an important question. Why does the bookmaker increase their betting limits as game time comes closer? The bets that players are placing with a bookmaker are essentially something similar to a voting mechanism. The more bets a bookie has collected, the more information it has about the different viewpoints concerning the event at hand.

Of course, this is not a democratic process since not all votes are created equal. As mentioned above, the size of the bet and the history of the punter are decisive factors as to how seriously the bookmaker will take the bet and what influence it will have on the line. But by and large, as more money flows into the market, the more confident the bookmaker becomes about their current number.

The invisible hand of the market

Essentially, a betting event is a market, where the bookmaker and all the punters are the market participants. Opening a line, a bookmaker is opening this market and is ready to take trades on this market from other market participants. It is willing to sell to you a Team A win or buy a Team A win from you. Of course, it will do so at a different price in order to make some profit on those transactions. The spread between the two prices is the vig. You can see what the vig for a market is when you calculate how much you are going to lose if you bet on all possible outcomes. You have bought and sold a possible outcome ensuring the same return for you regardless of how the game ends. The bookmaker is pocketing the spread.

A betting event fits the definition of a market pretty nicely. The market forces are the ones creating the price of an event. Therefore, the bookmakers that play a leading role in this process (which are often the same bookies that open the line) are called market makers.

The soft bookmaker

The market maker bookmaker business model is an important one for the betting environment but is also not the only one, and not even the most popular one. The biggest bookmaker brands follow a different model. They invest more in marketing to attract as many square punters as possible. They offer generous bonuses to punters and have sponsorship deals with big sports franchises.

On the other hand, those bookmakers do not invest that much in having a perfect line. Such bookmakers wouldn't want to take on the risk of opening the line for an event. They would often copy the market makers' lines on most events. They also wouldn't immediately move the line upon every single bet. Making a market is not their business. Therefore, their lines are not always the sharpest ones and they are sometimes referred to as soft bookmakers. Eventually, those bookmakers catch up with the market maker's line after a line move, but only after a certain delay, which offers a window of opportunity for the arber / value bettor.

So while a soft bookmaker will not follow the principles of market making as strictly as a sharp one, still, by and large, they pay respect to them. Their limits also increase come game time. Any discrepancy between their and the market maker's odds rarely lasts longer than a couple of minutes, after which the soft bookmaker adjusts.

The betting landscape

Different bookmakers have different lines – otherwise, technical value betting wouldn't exist. Even if they are not exactly the same, those lines are deeply connected. At the end of the day, the line of an event is a very homogenous product being offered by different providers at different prices. Thus, arbitrage opportunities arise and even those prices are out. Arbitrage and value betting providers like RebelBetting facilitate that process.

Therefore, the line on a certain event moves more or less synchronously between different bookmakers (save for the occasional time delay at soft books as mentioned above). What is causing this synchronous movement across bookmakers is the invisible hand of the market. The line at any given time represents the market consensus. In general, the bigger the market (in terms of the total volume of bets), the more accurate the price.

Price discovery

Given that the lines across bookmakers are connected, it is not only the betting volume in one bookmaker but in all bookmakers as a total that shapes the line. As time goes by, the wagered total gets larger, bookies grow more confident in their line increasing the limits, which attracts even larger bets from the sharks who wouldn't bother with the small limits. Therefore, the less time remaining to game time, the more accurate the line will be. This in turn means, that the line at game time (a.k.a. the closing line) is the most accurate line there could be.

Throughout its lifecycle, the line only gets more accurate with the closing line being the most accurate one. What are the implications of this finding?

The closing line as an indicator

We have mentioned that some bookmakers have sharp lines and some have softer lines. The softer lines represent an opportunity for the bettor. However, while some books are known market makers, not all of their lines are necessarily very sharp, especially at (or close to) opening. The difference is not always clear cut and it is not easy to find out whether the bet we've made is good or not.

This is where the closing line comes in. Remember, the price at closing is in fact the "accurate" price. Evaluating our bet is easy – we must simply compare it with the closing line. If we got a better price for our bet than we would have had if we had bet at closing, we have made a good bet. This "better price" is also referred to as closing line value or CLV. Having CLV on a long series of bets means that you are on the right track and even if variance has eaten into your bank, you can be confident that in the long run you will be profitable.

No profit first month?

Get Another Month Free.

If you don't make a betting profit in your first month, you get another month free.

Again and again until you profit. We take all the risk.

Technical value betting

There are some simple but effective strategies that reliably produce CLV over the long run. Technical value betting (the strategy supported by the value betting service of RebelBetting) is one such example.

Brand name bookmakers usually take a little bit of time to replicate the line movement of a market maker book. This delay opens up a window of opportunity for the bettor. Often the line movement at a market maker would be caused by new information entering the market, such as that an important player from one team has been injured at training. Being able to bet the opposing team at the price that was available before the news came out is a great advantage. That is what RebelBetting is offering to its customers. It is also important to avoid selection bias when value betting, to increase long-term profits.

Volatility expected

As in all betting strategies, the volatility of returns can be huge, especially over a shorter bet series. However, in the long run, the return on investment will tend to gravitate towards the CLV of your bets – this is especially the case with a clear-cut strategy such as the one RebelBetting is offering.

How do you calculate the CLV?

The expected return of your bet should be similar to your CLV, which in turn is strongly affected by the closing line. The formula for calculating CLV is the following:

Stake * (Odds taken / (Closing Odds * (1 + Margin)) – 1)

The margin (also called juice, vig) is calculated as:

1/Odds_1 + 1/Odds_2 + … + 1/Odds_n – 1

Above I calculate the fair odds using the simplified formula Fair Odds = Odds * (1 + Margin).

If you want to be exact you can take Joseph Buchdahl's formula (for a 2-way market):

Fair Odds = 2 * Odds / (2 – Odds * Margin)

For a 3-way market simply use 3 instead of 2. This one is accounting for the favourite-longshot bias. But you should come along just fine with the simple formula above.

The CLV in ValueBetting

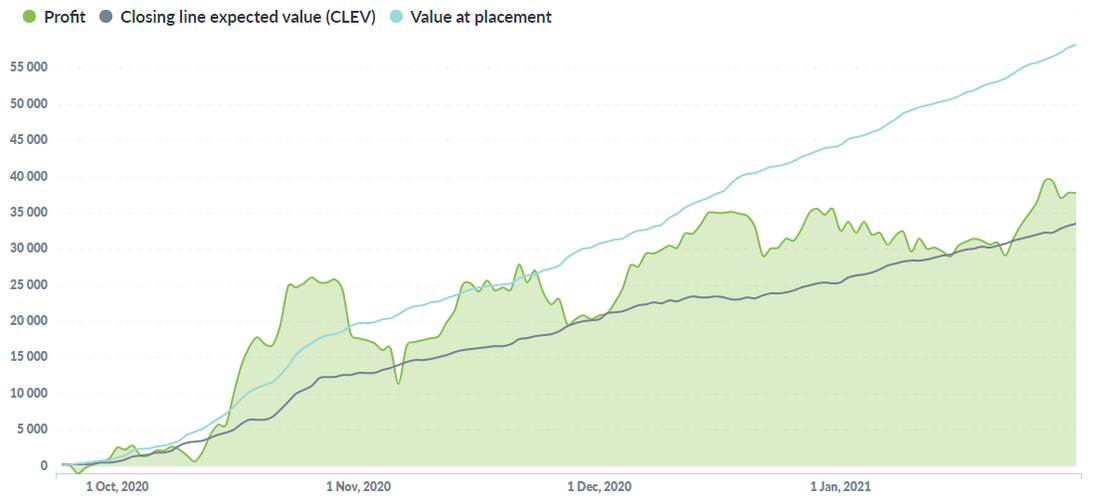

The value betting service stores the Closing Line Value for all your placed value bets. It's visible both at the top of the BetTracker and on your Reports page:

You can see that the profit curve (green) closely follows the CLV (blue). The value at bet placement (turquoise) is shown for completeness' sake – it will always increase more than the CLV, and is a less important metric.

However, one could argue, that perhaps sometimes it is not the soft bookmaker where you placed the bet that is in the wrong, but the sharp bookmaker and their closing line. We have seen above that in theory that shouldn't be the case, but perhaps this is not telling the whole story. And if that were the case, such methodology cannot reliably identify value.

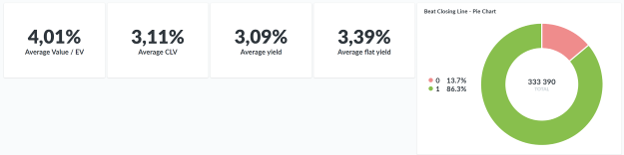

Fortunately, there is a way to test this. Let's analyze the closing line value of the first 333,390 bets generated with the ValueBetting platform. Let us have a look:

We see that 86.3% of the platform's bets have generated CLV. The average CLV has been 3.11%, in line with the average yield. Of course, you could have increased that if you focused on larger value bets.

The average flat yield percentage (resulting from level staking) is a bit larger. This is because when flat staking you won't turn over as much money and therefore the yield (profit/turnover) is higher. Your profits will be lower when flat staking, however.

The value at bet placement is 4.01% and will be 7 times out of 10 higher than the CLV. The main reason is the margins shrink as we get closer to the match start.

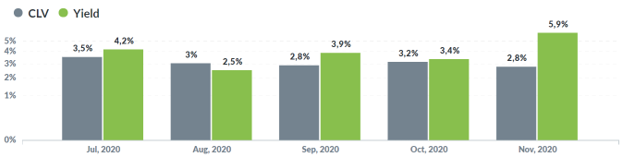

We can also see that:

1. Value betting reliably identifies a value, as measured by the closing line

2. The closing line value is in line with the achieved yield

Those two findings confirm that with a long enough bet record everyone can make a profit with value betting. The RebelBetting team also publishes the accumulated results of their users, which is showing pretty much the same thing.

Get started with RebelBetting

Get instant access to value bets and sure bets identified in real time. Built to help you find consistent, long-term profits - without guessing.

REBELBETTING TRIAL

14-day free trial — no credit card required

WHAT YOU GET

Value bets & sure bets

Bet tracking & auto settlement

100+ bookmakers

Basic access (limited features)

50 bets per day

REBELBETTING STARTER

Everything you need to profit

WHAT YOU GET

Value bets & sure bets

Bet tracking & auto settlement

100+ bookmakers

Unlimited bets per day

Built for consistent monthly profits

Higher value & sure bet limits

REBELBETTING PRO

Built for maximum volume & profits

WHAT YOU GET

Higher limits. Bigger profits.

Brokers (higher limits)

Access to sharp bookmakers

Access to betting exchanges

Unlimited profit potential

REBELBETTING STARTER 1 YEAR

Everything you need to profit

WHAT YOU GET

Value bets & sure bets

Bet tracking & auto settlement

100+ bookmakers

Unlimited bets per day

Built for consistent monthly profits

Higher value & sure bet limits

REBELBETTING PRO 1 YEAR

Built for maximum volume & profits

WHAT YOU GET

Higher limits. Bigger profits.

Brokers (higher limits)

Access to sharp bookmakers

Access to betting exchanges

Unlimited profit potential

Can I cancel my subscription at any time?

Yes. You can cancel future payments at any time and keep using the service until your subscription expires.

How can I be sure that I will profit?

You are always covered by our Profit Guarantee. If you don't make a profit the first month, you get another month for free – again and again until you profit!

Conclusion

What if I lose money even with positive CLV?

Short-term variance is normal. But with a large enough sample, CLV always wins. That's why we track it.

How can I be sure RebelBetting works?

Over €20,287,195 total member profits, over 16 years online, and thousands of users prove the strategy. Plus, our Profit Guarantee removes the risk.

Do I need betting experience to use RebelBetting?

Not at all. Beginners and pros alike use the software successfully. We also have loads of free educational resources available.

Can bookmakers limit me?

Yes, eventually. But our guides and community show you how to stay ahead with multiple accounts and brokers.

With the above, I hope to have convinced you of the importance of the closing line in betting. I feel many punters can greatly improve their results (which for most translates simply to losing less) by understanding this concept and tracking their CLV. There are exceptions to every rule, but for most people, dropping the bets that have a negative CLV would have very positive effects on their bank accounts. The ability of value betting to consistently generate +CLV bets is its strongest asset and what makes technical value betting a viable strategy. I urge anyone not to take my statement at face value and check for themselves.

For more interesting articles, see the value betting help section.