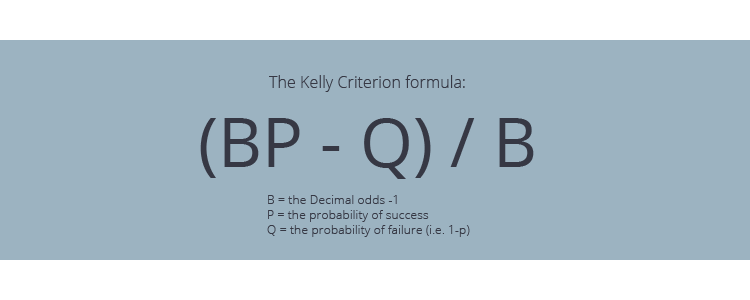

Kelly criterion for stake sizing

Fractional Kelly

The Kelly criterion is a staking strategy that calculates the optimal stake for maximum long-term growth of your bankroll, based on the value of the bet.

It is a scientific betting method that is mathematically proven to lead to higher wealth generation than any other strategy in the long run. It was first described by J. L. Kelly Jr, a researcher at Bell Labs, in 1956.

We use the Kelly criterion when recommending the optimal stake when you're betting on value bets.

Fractional Kelly

The full Kelly criterion suggests that a bettor should wager a percentage of their bankroll equal to the expected edge divided by the odds, which is often a very aggressive strategy.

In the case of sports betting, the expected edge is often difficult to accurately estimate, and the odds can be very volatile. As a result, using the full Kelly criterion can be very risky and lead to excessive losses, even with a significant edge.

On the other hand, a fractional Kelly criterion (betting only a fraction of the optimal full Kelly bet size) can provide a more conservative approach to bankroll management. By betting a smaller percentage of the optimal bet size, bettors can reduce the risk of large downswings while still maintaining a positive expected value over the long run. Therefore, in sports betting, it is generally recommended to use the fractional Kelly criterion rather than the full Kelly criterion in order to manage risk and maintain a steady growth of your bankroll.

You want to find a comfortable balance between expected profit and money risked. Decreasing the Kelly percentage will decrease your downswings, while only decreasing your profits very slightly.

30% Kelly is the default setting in RebelBetting and hits a good balance between profit and risk.

We recommend 20% when you're starting out with a small bankroll or just want to decrease the risk of large downswings. You can change this by going to Options. But before you do, please make sure you have understood how your Kelly stake sizing affects variance.

Using a Kelly above 50% is not recommended and will lead to very high variance and steeper draw-downs, with very little increase in profits.

Fractional Kelly stake sizing can also be combined with a max bet size.

Kelly and multiple simultaneous bets

The original Kelly criterion is proven to be mathematically optimal when placing a single bet, an infinite number of times. In reality, your goal is to maximize your expected bankroll growth over a finite number of bets, often having many simultaneous bets open.

Automatically adjust bankroll for open bets

When you have many open bets, they must be subtracted from your effective bankroll used when calculating the Kelly stake size for the next bet, to maintain the same risk level.

This is especially important if you often bet a majority of your bankroll each day. If you have 50 open bets and bet the same amount on every bet, you are effectively ignoring the Kelly criterion, resulting in high variance.

On the other hand, if you only bet 10% of your bankroll every day, you will not notice much difference. The feature can be turned off in Options, just disable "Adjust for open bets".

In RebelBetting, we calculate this adjusted bankroll automatically for you. Just keep the checkbox "Adjust for open bets" enabled in Options (it's enabled by default). This will slowly decrease the recommended stake as the number of open bets increases, helping you manage your risk while optimizing your profits.

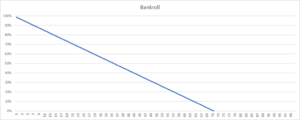

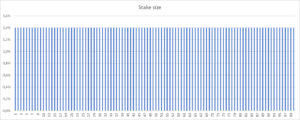

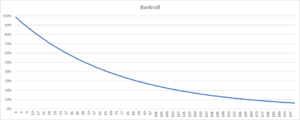

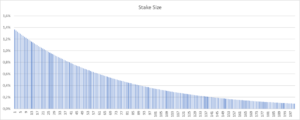

Comparison charts

Here you can see how your bet size and bankroll will change when adjusting for open bets or not. In the example, we're having multiple 5% value bets open simultaneously.

Without adjusting for open bets

Here you bet the full "single bet Kelly" percentage of 1,4% on every bet. You can place 70 bets before your bankroll is fully turned over. You notice there is no decrease in bet size (and risk) even though your effective bankroll decreases.

When adjusting your bankroll for open bets

Here the bet size is decreasing together with the bankroll. Note that maintaining a proper Kelly criterion means lower risk, lower variance and smaller drawdowns, but also slightly less average profit. Your bankroll will never run out, since the strict Kelly criterion will never suggest you bet your entire remaining bankroll.

Kelly Stake Sizing strategy vs Flat staking

The Kelly staking strategy is generally considered to be a better option than flat staking when value betting because it allows you to adjust your bet size based on your estimated edge over the market.

This means that if you have a high edge, you can increase the stake; whereas, if you have a low edge, you can reduce the stake. By adapting your stake size in this way, you are able to maximize your profits and minimize your losses over time. Check out the video to learn more: